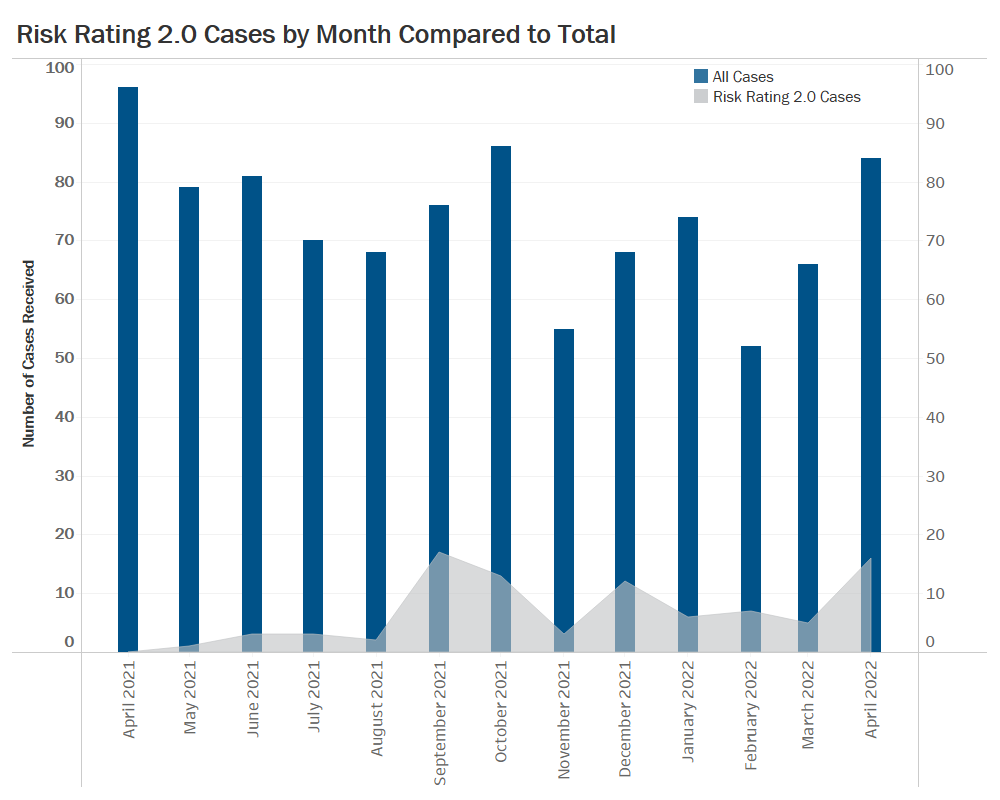

Risk Rating 2.0 Impact on OFIA Casework

Risk Rating 2.0 FAQs

Casework Spotlight

The Office of the Flood Insurance Advocate (OFIA) publishes its periodic report to provide the public and industry professionals an insight into trends affecting National Flood Insurance Program (NFIP) customers and property owners.

Risk Rating 2.0 Impact on OFIA Casework

Since its creation under the Homeowners Flood Insurance Affordability Act of 2014 (HFIAA), the Office of the Flood Insurance Advocate (OFIA) has fielded thousands of inquiries from policyholders and property owners asking:

- Is the flood insurance premium that I was quoted correct?

- If the flood insurance premium is correct, why it is so high?

- What can I do to reduce my flood insurance premium?

In response to these inquiries, OFIA aids policyholders in obtaining and verifying accurate and reliable flood insurance rate information when purchasing or renewing a flood insurance policy. OFIA also educates property owners and policyholders under the National Flood Insurance Program (NFIP) on their individual flood risk, and measures to reduce flood insurance rates through effective mitigation.

Risk Rating 2.0 is the first major overhaul of the NFIP’s flood insurance rating methodology in over fifty years. This new rating methodology produces flood insurance premiums which more accurately reflect a property’s risk. OFIA anticipated an increase in inquiries related to Risk Rating 2.0, however, to date there has not been a spike in RR2.0 casework.

Risk Rating 2.0 FAQs

The inquiries OFIA receives related to Risk Rating 2.0 are categorical questions that impact a broader base of policyholders, and through coordination with FEMA’s Underwriting Branch, and Actuarial and Catastrophic Modeling Branch, OFIA has developed the following responses to address these questions. OFIA also refers inquirers to the Risk Rating 2.0 website and FEMA’s regularly updated Frequently Asked Questions document.

I don’t see the discounts I expected. How is the premium calculated?

In the new methodology, the full-risk premium is calculated based on the inputs provided.

An individual policyholder's premium may be less than the full-risk premium either due to statutorily-mandated discounts, such as Pre-FIRM or Newly Mapped, or due to the statutory annual increase cap (18% in most cases).

FEMA’s Federal Insurance Directorate (FID) has produced a “Discount Explanation Guide” that provides details on how many of these discounts are calculated and applied.

While this topic still confuses many, OFIA is committed to working with the program offices to continue developing communication materials which better explain how premiums and discounts are calculated and applied.

Why is my renewal more than 18% higher than last year?

For most policyholders under Risk Rating 2.0, there is a legislative cap on annual premium rate increases of 18% per year. Some policyholders may notice a premium increase which appears to exceed the 18% cap because of fees and surcharges, which are not subject to the statutory cap under the law. FEMA has kept all fees and surcharges constant for standard rated policies transitioning to Risk Rating 2.0.

However, with the elimination of the Preferred Risk Policy (PRP), policyholders transitioning from a PRP to a standard policy under Risk Rating 2.0 are seeing an increase in the Federal Policy Fee from $25 to $47. Because the 18% increase cap is applied before the fees are added, it can appear that the 18% cap has been exceeded by $22.

Increasing the amount of coverage, decreasing deductibles, or losing discounts due to a downgrade in the community’s Community Rating System (CRS) classification can also give the appearance that a premium is increasing in excess of the 18% cap.

Certain pre-FIRM (built before Flood Insurance Rate Maps) properties are subject to a 25% statutory cap; namely, policies covering non-primary residences, businesses, and Severe Repetitive Loss, cumulative loss, or substantially damaged properties.

My Risk Rating 2.0 renewal price went down substantially. Was I overpaying previously?

The new rating methodology cannot be applied retroactively, and a premium decrease under Risk Rating 2.0 does not always indicate that a policy was previously misrated in the old methodology. Nonetheless, in instances where there was a misrating, OFIA has helped some customers obtain up to five years of refunded premiums. Common things to verify in the old rate methodology are primary residency status, basic building description, such as whether a building has a basement or not, and mapping information such as the Flood Zone.

As an agent, I'm seeing quotes in the new methodology that are higher than the old methodology. Is this correct?

Risk Rating 2.0 produces premiums which more accurately reflect a property’s unique risk. It is inaccurate to compare policies under the new, more accurate methodology, to those which were calculated under the old methodology, as those premiums did not necessarily reflect the true risk of the property.

Where high risk and high value intersect, generally seen in areas where buildings are closest to flood sources, premiums of under $1,000 are no longer available. This is true for many coastal homes, even in X Zones near the boundary of a Special Flood Hazard Area. Coastal A Zones may be priced more like the old V zones.

For buildings further from the flood source, maximum coverage can now be purchased for lower value homes at a lower cost than the old Preferred Risk Policy. Pre-FIRM discounted policies, condominium policies, and commercial policies are also generally experiencing premium rate reductions.

In validating a Risk Rating 2.0 price, an agent should verify the correct address, foundation type, and square footage, as well as utilize elevation information if available. Assuming all inputs are correct, the largest increases for new business quotes occurs for homes closest to a flood source and with the highest replacement cost values.

Has FEMA learned anything from Risk Rating 2.0 inquiries?

Yes. FEMA has developed procedures and processes to ensure the new methodology is accurate. FEMA has made minor adjustments to apply more recent topographic and replacement cost value data and has worked with insurers where needed to address rating discrepancies. Additionally, based on our learnings from various stakeholders, FEMA has created new tools such as a Rate Explanation Guide, Discount Explanation Guide, Agent Simple Guides and training videos to improve understanding.

Casework Spotlight

Customer Issue

A policyholder from New Jersey reached out to the OFIA inquiring if future mitigation projects could help reduce their $13,144 flood insurance premium. When asked, it was discovered they had never given their Elevation Certificate (EC) to their insurance carrier.

Background

OFIA worked with the customer’s insurance carrier while keeping FEMA’s NFIP Direct Servicing component apprised of any developments. Upon a review of the EC, it became apparent the building had been misrated. The insurance carrier updated the building description and corrected the misrating.

Resolution

With the correct rating of the building established, the carrier issued refunds for the last five years, which is the maximum refund allowable due to a misrating. The refunds totaled $23,366. The annual premium was also reduced to $4,680 under the Risk Rating 2.0 methodology.

What We Heard From NFIP Customers

“Your Advocate Representative did an OUTSTANDING job solving my problem. They were kind, courteous, and efficient. I am so appreciative of the 'rescue' I got from this office. My nightmare is over! Thank you!”