OFIA Casework Highlights

OFIA Casework Outlook

Casework Spotlight

The Office of the Flood Insurance Advocate (OFIA) publishes its periodic report to provide the public and industry professionals an insight into trends affecting National Flood Insurance Program (NFIP) customers and property owners.

OFIA Casework Highlights

Since 2015, the OFIA has advocated for NFIP policyholders with compassion and fairness. During this reporting period, the OFIA resolved 92% of new inquiries. A beneficial outcome has been received by 47% of our inquirers.

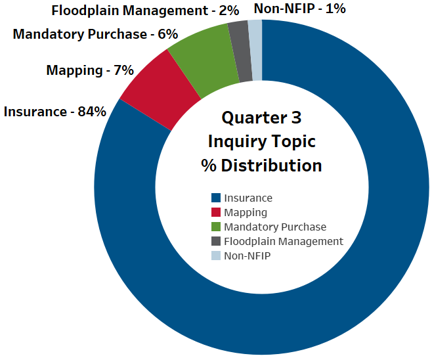

From Quarter 2 to Quarter 3, the OFIA has seen a 6% increase in the number of insurance-related inquiries, a 4% decrease in the number of inquiries related to the federal flood insurance requirement, and a 3% decrease in the number of inquiries about floodplain management regulations and procedures.

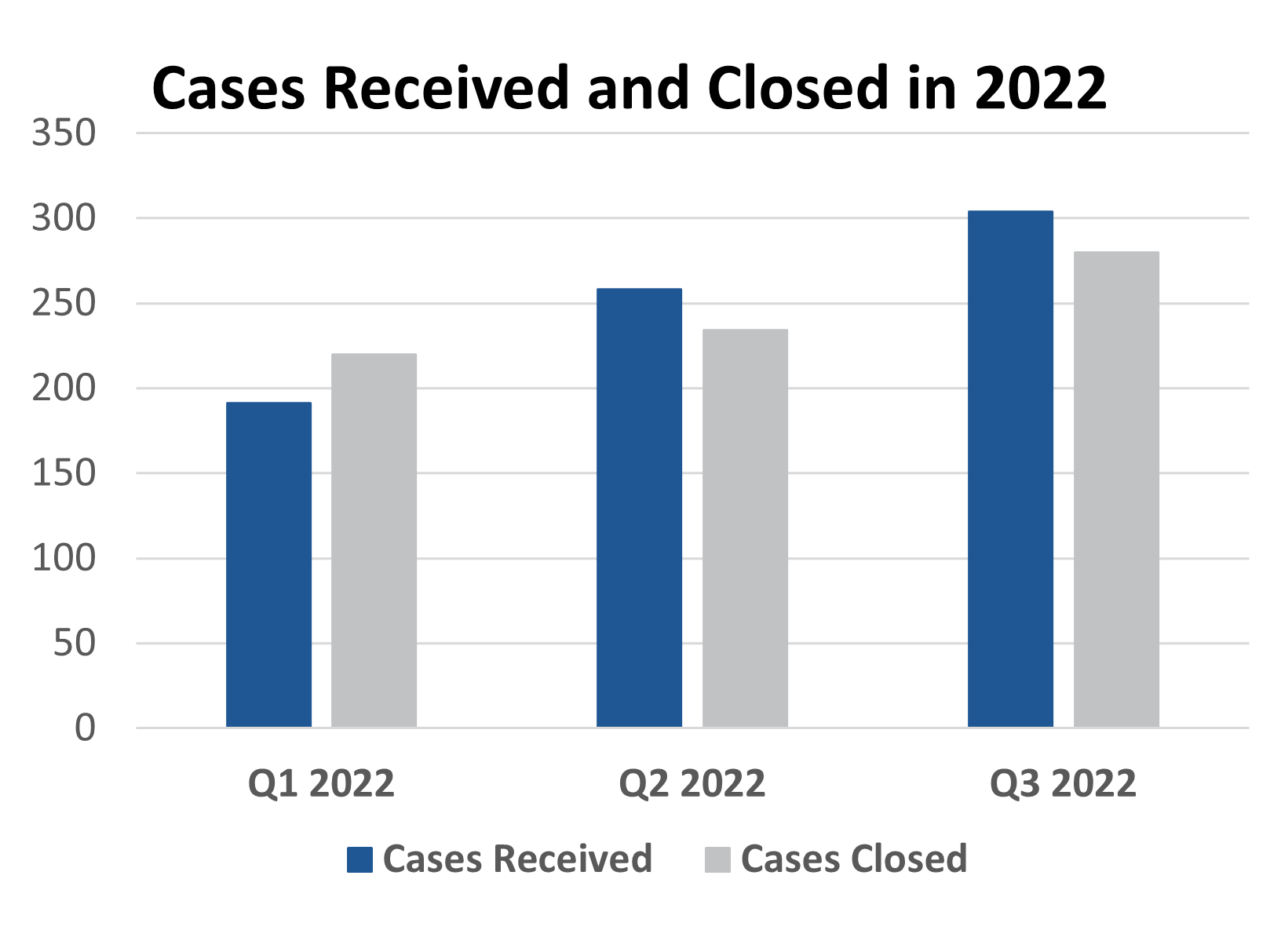

- In Quarter 3, the OFIA received and closed a record number of inquiries.

- Compared to Quarter 2, Quarter 3 reflected an 18% increase in the number of cases received and a 20% increase in the number of cases closed.

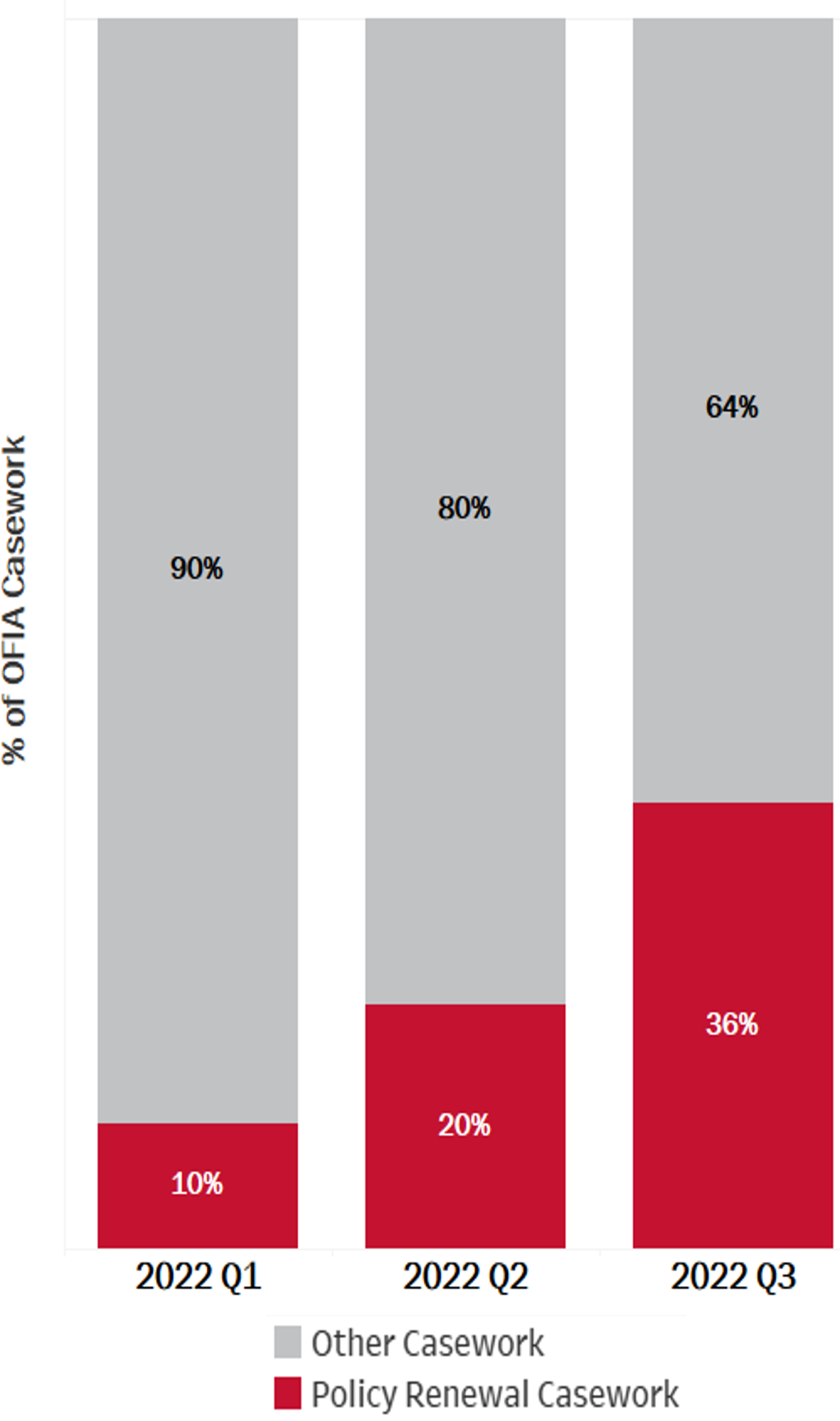

Policy Renewal vs. Other Casework

- As more flood insurance policies continue to transition from the legacy rating system into Risk Rating 2.0 policies, the OFIA continues to see an increase in both the volume and percentage of inquiries related to the renewal of NFIP policies.

- Most of our policy renewal casework involves policies that have not renewed within the 30-day grace period, which results in a policy lapse.

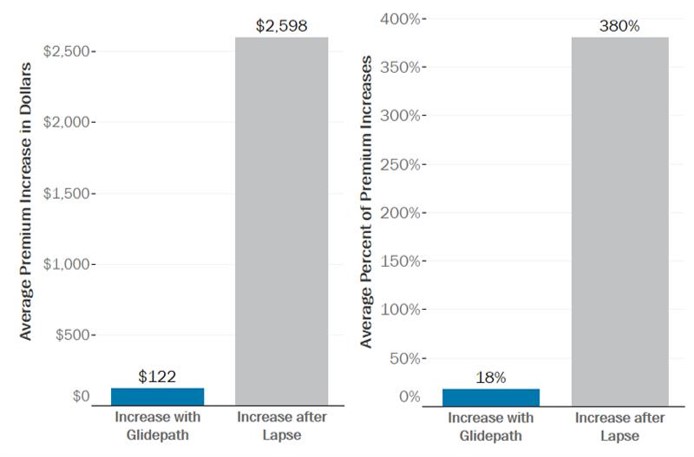

Consequences of a Policy Lapse

- When an existing policy renews into Risk Rating 2.0, the premium increases each year by 18% until it reaches the full-risk premium. We call this gradual increase "the glidepath." If a policy lapses, the glidepath is lost and the full-risk premium is immediately charged.

- Based on a review of 30 cases from Quarter 3, the average first-year premium increase for existing policies renewing as Risk Rating 2.0 policies was $122 (18%) with the glidepath and $2,598 (380%) without the glidepath

- It is important to note that 30 cases does not represent all NFIP policyholders. Policyholders reaching out to OFIA are usually those most adversely impacted by a lapse.

National Flood Insurance Program (NFIP) Flood Insurance Claims

On average, just under 20% of annual inquiries to the OFIA are related to NFIP flood insurance claims. The OFIA anticipates an increase in claims-related inquiries as we move into Quarter 4 and as NFIP policyholders begin the process of repairing damage from storms that occur during the second half of this hurricane season.

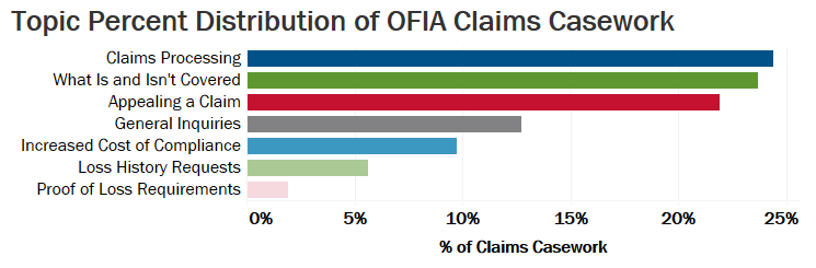

As shown in the chart below, the OFIA responds to a broad range of claims-related inquiries from NFIP policyholders.

Types of Claims Questions from OFIA Casework

- Claims Processing: These are questions about navigating the claims process.

- What is and Is Not Covered: These are requests for basic information about the terms and conditions of the Standard Flood Insurance Policy (SFIP).

- Appealing a Claim: These are request for information about how to appeal a claims settlement decision.

- General Inquiries: These are requests for general information such as mailing addresses.

- Increased Cost of Compliance: These are questions about Coverage D of the SFIP.

- Loss History Requests: Policyholders seek information about the history of flood claims to their property.

- Proof of Loss Requirements: These are specific questions about how to complete a proof of loss.

OFIA Casework Outlook

Overview of the Claims Process

The OFIA created this video to help the public better understand how to navigate the claims process for policies under the NFIP.

Additional Claims Tips for NFIP Policyholders

- The NFIP’s Summary of Coverage publication summarizes which items are and aren’t covered under an NFIP policy; for a complete list, refer to your policy documentation

- Make a complete list of all your damaged items and take pictures and/or video of everything; be prepared to prove when you purchased damaged items and to show proof of purchase

- Write down all questions that you have for your adjuster ahead of the inspection and ensure that all your questions are answered

- Make sure you keep copies of all documentation related to the processing of your claim

Additional Claims Resources for NFIP Policyholders

We encourage everyone to help spread the following messages to help policyholders avoid lapses and maintain continuous coverage:

Casework Spotlight

Customer Issue

An NFIP policyholder from New York demolished and rebuilt a home according to NFIP requirements. The new Elevation Certificate was provided to the insurance company, but the insurance premium was not lowered as a result of the mitigation efforts.

Background

The OFIA reviewed the Elevation Certificate and the policy rating details and noticed potential discrepancies with the foundation type, flood openings, and location of machinery and equipment.

Resolution

The OFIA collaborated with the land surveyor and the policyholder to verify Elevation Certificate data and rating inputs and helped the policyholder provide clarifying documentation to the insurance company. The insurance company rewrote the policy and the new premium resulted in $500 savings for the policyholder.

What We Heard From NFIP Customers

“The Advocate Representative went above and beyond to fix my problem, following up several times with my insurance company and me to make sure things were on track. I have literally never had a better experience with a federal agency in my life than this one.”

Need Help?

After using the available NFIP resources, if you still have questions, visit our Flood Insurance Advocate webpage and click “Ask the Advocate.”