OFIA Casework Highlights

OFIA Casework Trends

Casework Spotlight

The Office of the Flood Insurance Advocate (OFIA) publishes its periodic report to provide the public and industry professionals an insight into trends affecting National Flood Insurance Program (NFIP) customers and property owners.

OFIA Casework Highlights

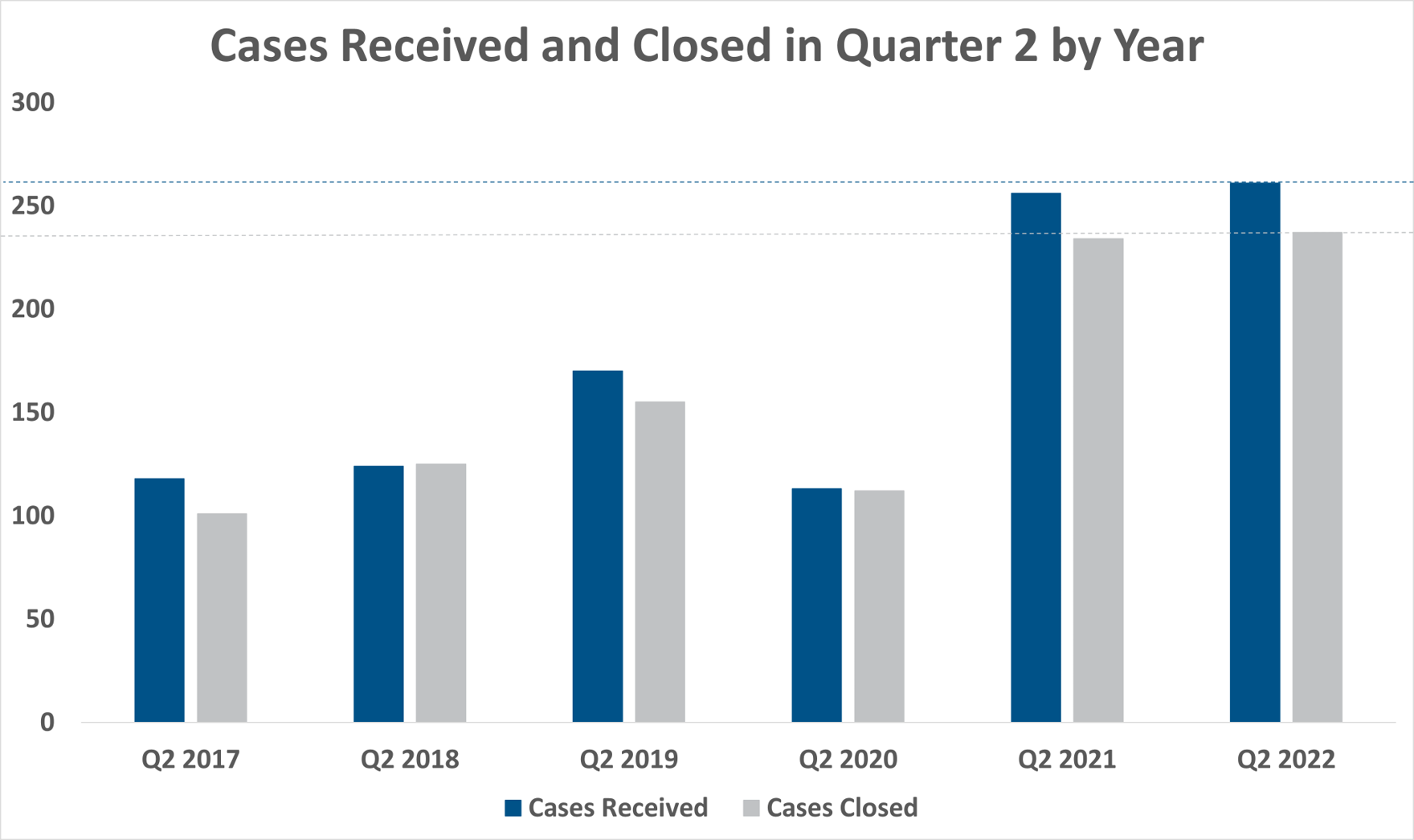

- In Quarter 2 2022, the OFIA received and closed a record high number of cases in a quarter

- The OFIA received 36% more cases and closed 8% more cases in Quarter 2 2022 than in Quarter 1 2022

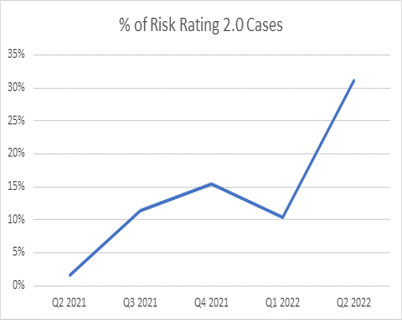

- The proportion of Risk Rating 2.0 cases has increased three-fold from Q1 to Q2 2022

- As more people renew their policies under Risk Rating 2.0, OFIA is receiving more inquiries about the transition to the new methodology

OFIA Casework Trends

Increases in “Legacy Rating to Risk Rating 2.0” Inquiries

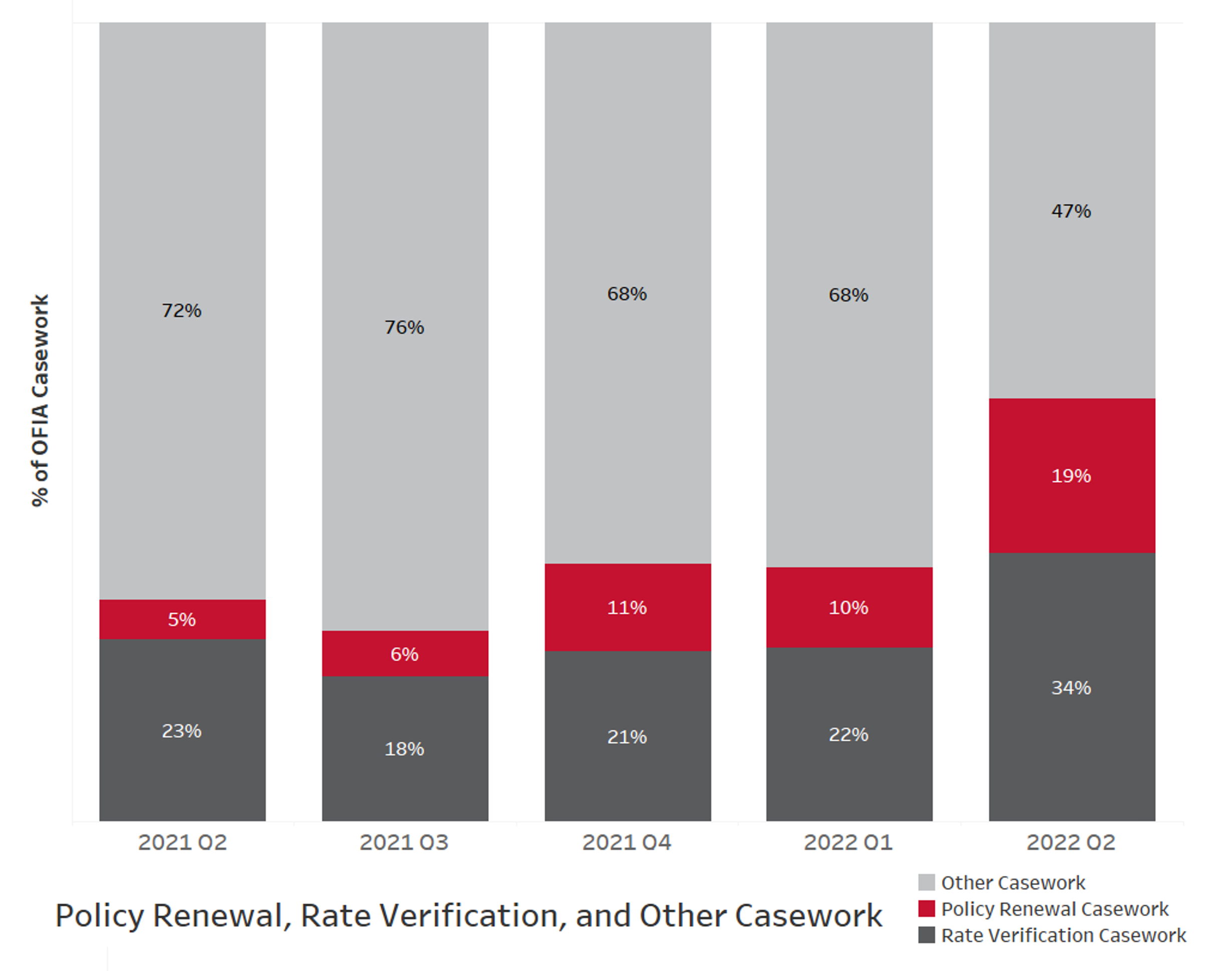

In Quarter 2, the OFIA saw an increase in the number of inquiries related to the renewal of National Flood Insurance Program (NFIP) policies transitioning from the legacy rating system to Risk Rating 2.0.

In Quarter 2 of 2021 only 5% of inquiries were about policy renewal topics. By Quarter 4 of 2021 the percentage increased to 11%, and it reached 19% in Quarter 2 of 2022.

This correlates with the implementation of Phase 2 of Risk Rating 2.0 at the beginning of the quarter, which impacts policy renewals.

The OFIA also saw an increase in rate verification casework, primarily related to pricing under the Risk Rating 2.0 methodology.

Risk Rating 2.0 Glidepath Discounts Lost after Policy Lapses

Most policy renewal inquiries are about policies that have lapsed because the renewal premium was not paid prior to the end of the 30-day grace period. In Quarter 2, this type of inquiry made up 50% of policy renewal casework and 14% of OFIA’s overall casework.

Policies have lapsed for the following reasons:

- Policyholder’s inability to pay due to personal financial hardship

- Renewal bills not received because of mail delays

- Renewal bills sent to the incorrect mailing address

- Payment processing discrepancies

- Lender servicing confusion

The Impact of Policy Lapses

Under Risk Rating 2.0, some policyholders receive glidepath discounts which limit annual policy increases to 18%. In some cases, the loss of glidepath discounts due to a policy lapse can mean a premium increase of thousands of dollars. This can be shocking and devastating news for a policyholder, especially when the policy lapsed because a policyholder was already struggling to pay the lower premium amount.

Best Practices for Policyholders

We encourage everyone to help spread the following messages to help policyholders avoid lapses and maintain continuous coverage:

- Ensure that other parties responsible for submitting the renewal payment have done so, such as a lender or insurance agent, including where you receive correspondence indicating “this is not a bill”

- Contact the insurer or agent to ensure that renewal bills are being sent to the correct address before the policy expires

- Policyholders paying directly should send the maximum they can afford, yet is close to what was billed, in order to avoid a lapse and to maintain eligibility for the glidepath discount, even if the coverage amount will be reduced

- Don’t wait until the last minute to check on the status of the renewal after payment has been made

Casework Spotlight

Customer Issue

The OFIA received an inquiry from a policyholder in New York who needed to understand why their rates continued to increase each year, even after they elevated their house in 2019. Their home was damaged by Irene in 2011, destroyed by Sandy in 2012, but had since been elevated under the NY State Build it Back program.

Background

The policyholder provided their Elevation Certificate (EC) and photos of the mitigated home which OFIA shared with FEMA’s Direct Service Agent Branch. The application of the EC resulted in a refund of $12,344 for the current term. Not completely satisfied with this result, the homeowner presented proof that their agent had submitted the EC to the NFIP the previous year. Unfortunately, the agent had sent the EC to an outdated NFIP Direct email address, so the EC was never received, nor applied.

Resolution

OFIA advocated for an additional year of refund, based on the building having been elevated in 2019, and the agent’s attempt to submit the Elevation Certificate in 2020. For these reasons, FEMA’s NFIP Direct Service Branch approved this request and issued another refund in the amount of $9,782.

What We Heard From NFIP Customers

“You ARE amazing! Please forgive me if I was rude at any point, sometimes I get exhausted 'battling' agencies. Thanks for your compassion, it is sometimes so sorely missing!”